Key Developments

- EAT Lancet report on food systems (see also) and G20 Food Security resolution highlighted the importance of market data and actions for fair markets

- We find food prices remain high and volatile in East and Southern Africa and cross-border markets continue to work very poorly

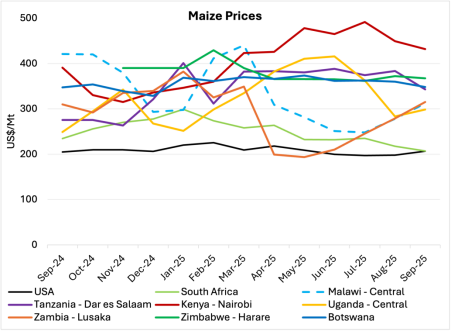

- Good maize harvests, especially in Zambia, have moderated prices somewhat across the region, although prices remain above US$400/Mt in Nairobi.

- Despite a much better harvest in 2025, Zimbabwean domestic maize production still falls short of national demand and the import ban imposed has now been lifted

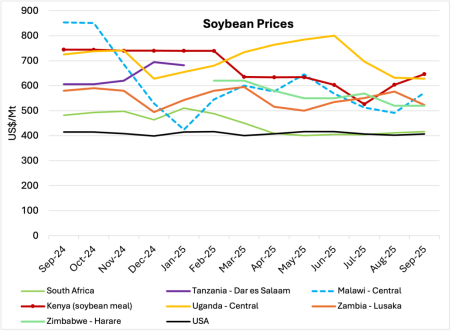

- Soybean and rice prices in East Africa remain extremely high

- Below-average rainfall is now expected across parts of eastern Africa until December 2025, driven by likely La Niña conditions beginning in September and projected to continue into early 2026.

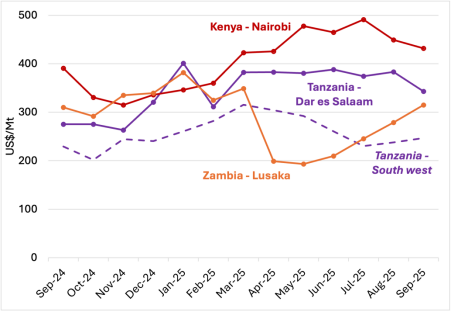

Maize developments

Figure 1: Maize prices, selected ESA countries.

1 – Source: AMO based on price tracker data from multiple sources.

- Kenya prices remain very high, far above supply areas in south-west Tanzania and Zambia although the gap has narrowed.

- Zambia prices increased after the export ban lifted in August, with prices more than 50% higher than at the harvest in April/May.

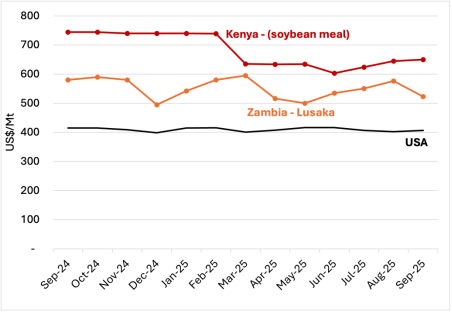

Soybean developments

Figure 2: Soybean prices, selected ESA countries

2 – Source: AMO based on price tracker data from multiple sources.

- Average prices in Kenya for soymeal have continued to increase to US$650 in September

- The Kenya average hides differences between larger regular buyers who have seen stable prices close to US$600/Mt, while smaller spot buyers have seen increases, with differences reaching US$130/Mt

- In local currency terms, Malawi prices have remained unchanged, and at the official exchange rate are high at US$1370/Mt (see annexure for Malawi chart); however, at the parallel exchange rate, pricing are lower albeit increased to US$594, likely reflecting exports to Nairobi

- Tanzania’s claim to export soybeans to China is inconsistent with low production, and it likely reflects re-exports from Malawi

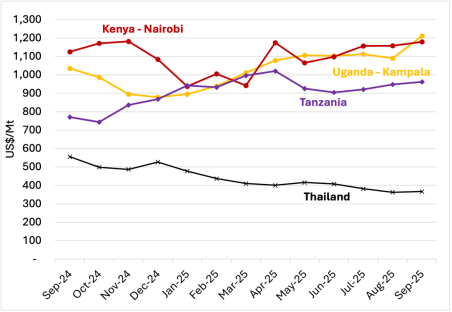

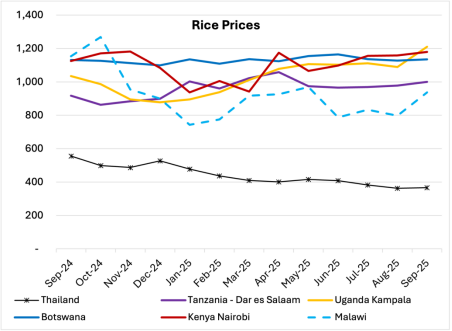

Rice Developments

Figure 3: Rice prices, selected ESA countries

3 – Source: AMO based on price tracker data from multiple sources, Thailand price is from the World Bank

- Rice prices in the region have continued to increase and are more than double world prices which have moderated

- Moves to reduce protection in Kenya have been contested in court

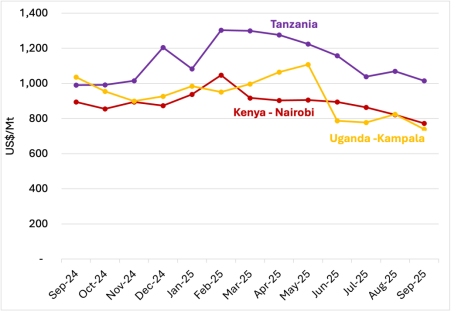

Common beans developments

Figure 4: Common Bean prices, selected ESA countries [1]

4 – Source: AMO based on price tracker data from multiple sources

[1] Uganda: K132, rosecoco and yellow beans. Rwanda: RWR 3194 and RWR 2245. Kenya: rosecoco, yellow-green beans, red haricot, mwitemania. Tanzania: red beans – uyole 96, lyamungo 98; lyamungo 95, yellow beans -selian 13, njano uyole; sugar beans – masipenjele

- Prices have moderated in Tanzania, Kenya and Uganda, although Tanzania remains substantially higher.

Detailed price charts –Selected ESA countries & International Prices

5 – Source:

AMO based on price tracker data from multiple sources, Malawi prices received in local currency and converted using the parallel exchange rate from November 2024 , as discussed

here. South Africa is SA Futures Exchange price; USA is fob prices from SAGIS.

6 – Source: AMO based on price tracker data from multiple sources, Malawi prices received in local currency and converted using the parallel exchange rate from November 2024, as discussed

here. South Africa is SA Futures Exchange price; USA is fob prices from SAGIS.

7 – Source: AMO based on price tracker data from multiple sources, Malawi prices received in local currency and converted using the parallel exchange rate from November 2024, as discussed

here. World price is from the World Bank.

African Market Observatory AMO