The culmination of the initial short harvest season transpired in August; however, the supply of numerous items had been previously recorded in June and July. A significant portion of the commodities is presently held in the custody of the trading community, which consists of rural assemblers, transit traders, and stockists. Many harvested commodities have recorded their lowest price this season and are already beginning to ascend as stocks continue to dwindle.

A substantial quantity of beans has been delivered to the market from various production locations across the country. Freshly harvested beans have finally been documented from the western and northern regions this season. Bean prices fluctuated between Ugx. 2,400 and 3,000 per kilogram at wholesale from June to August. Prices are anticipated to escalate in the near future as the final school term of the year begining in September.

The maize grain harvest has also commenced, with prices recorded at a low of Ugx. 1,000 per kilogram in Kampala during August, compared to Ugx. 1,520 per kilogram in May, which marked the peak of the second and final season for 2024. The demand for unsorted maize grain remains robust, particularly in Kenya, at regional level. The current harvest has rendered maize cheaper compared to that sourced from Tanzania, part of which was subsequently delivered to Uganda via Mutukula. The grain price is also expected to rise as the school term begins.

In rural production areas such as Hoima, Kiboga, Masindi, Mubende, Kabarole, Kyegegwa, and Iganga, maize was offered at a low price of Ugx. 700-900 per kilogram at wholesale, contingent upon quality, quantity, and location.

An increase in the price of Super rice was noted during August. A notable degree of adulteration of rice was observed, enabling Super rice traders to bolster their profit margins. Supply from Tanzania continues to command a significant share of the Ugandan rice market. Grade One Super rice saw a reduction in quantity, with prices rising from Ugx. 3,500 per kilogram to Ugx. 3,800-4,000 per kilogram for both 50 and 25-kilogram bags.

Other varieties, such as Kaiso and Upland rice, were considerably more affordable, priced at Ugx. 2,500-3,000 per kilogram at wholesale.

The harvesting of Irish potatoes in Kapchorwa has commenced, resulting in a decline in market prices to Ugx. 600-800 per kilogram in Kapchorwa. This supply has been distributed to several markets, including those in Kampala City. However, the market has also been receiving Irish potatoes from Kenya (Naivasha, Kisumu) in 110-140 kilogram sacks at a lower price, particularly demanded in the peri-urban areas along the Busia-Kampala road. In the well-established Kenyan transit traders’ market located in Kisenyi, Kampala, known as the “Bumonde Traders Association Stage,” Irish potatoes were offered at Ugx. 120,000-160,000 per bag. Supply from other production locations was less favored and considerably cheaper.

Other staple food supplies to major markets have been recorded regularly.

Regional outlook.

Demand for maize from Uganda to Kenya was low at 600-700 tons crossing formally on a daily Likewise 100-400 tons of assorted beans have found market in Kenya. Supply of beans was mainly recorded from Ethiopia and Tanzania

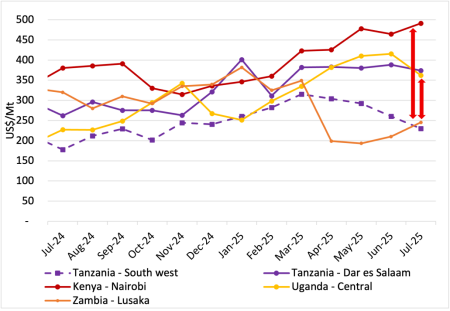

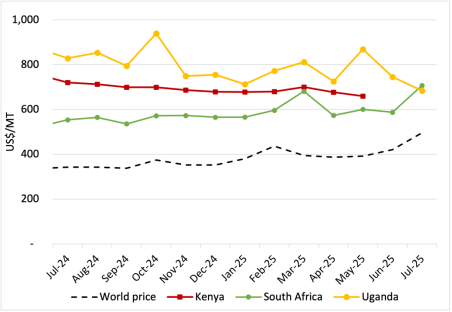

Maize prices, selected ESA countries.

AMO based on price tracker data from multiple sources.

- Prices in Kenya continue to increase ahead of October harvest and are 70% above import parity from Tanzania pointing to high trader profits

- Imports to Kenya are restrained by apparent ongoing Zambia export ban despite its good harvest, and claims of high aflatoxin on 30-40% of Tanzania imports

- High prices in Dar es Salaam point to substantial trader margins within Tanzania

- Prices in Zambia, where harvests were good meaning a substantial surplus, have improved somewhat to US$245/Mt in July just above Tanzania producing areas, perhaps in anticipation of the export ban being lifted, although it still means farmers getting much less than they could earn from export markets

- In Malawi prices declined to US$248/Mt at the parallel exchange rates, although much higher at official rates (see annexure for Malawi chart).

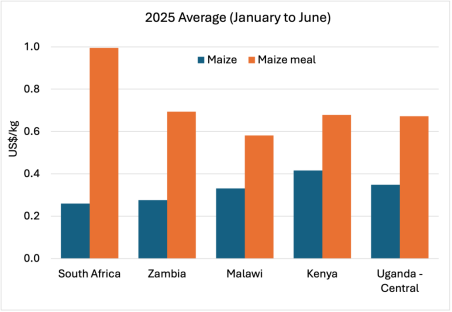

Zambia has high maize meal prices relative to maize prices in 2025.

- A substantial drop in maize prices in maize prices from March 2025 has not been reflected in declines in maize meal prices, suggesting market failures and/or market power impacting on price transmission along the value chain.

Malawi: maize meal prices have varied substantially over the 12 months while they were among the lowest of the selected countries in the first half of 2025, consistent with maize prices.

- Maize meal prices in Malawi seem to have greater seasonal variations tracking maize prices.

- Price trends depend on the exchange rates used (with parallel rates used in Figures below)

Kenya and Uganda: maize meal and maize prices follow similar trends

- Maize meal prices increased over year to June 2025, albeit at slower pace than maize prices.

- Kenya has by far the highest maize prices but this has not translated into the highest maize meal prices as Government interventions have eased price pressures

- Unfavourable weather conditions in Uganda have put pressure on food prices, including maize meal prices, likely a pass-through from surging maize prices.

Maize vs. maize meal prices, selected ESA countries

3 – Source: AMO based on price tracker data from multiple sources, Malawi prices received in local currency and converted using the parallel exchange rate from November 2024 to June 2025, as discussed here.

South Africa has had the lowest average maize prices among the selected countries (Figure below), yet it has the highest maize meal prices by far.

- Maize meal prices increased 13% in US$ terms over 12 months to May 2025, while maize prices reached a peak in January 2025 before easing back to 2024 levels over first half of 2025 (Figure below).

- Higher level of maize meal relative to maize prices could reflect higher retail costs and margins, as well as economies of scale and high barriers to entry in large-scale milling for highly refined maize meal.

- Divergence observed between maize and maize meal prices from January 2025 is consistent with a lag effects in price transmission and a ‘rockets and feathers’ effect.

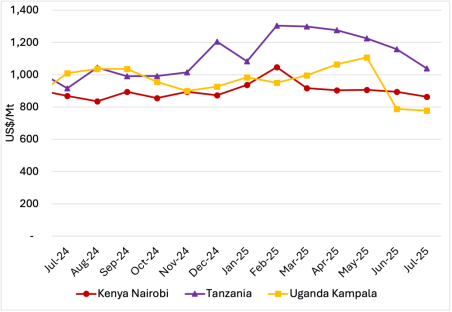

Beans prices, selected ESA countries.

AMO based on price tracker data from multiple sources

Uganda: K132, rosecoco and yellow beans. Rwanda: RWR 3194 and RWR 2245. Kenya: rosecoco, yellow-green beans, red haricot, mwitemania. Tanzania: red beans – uyole 96, lyamungo 98; lyamungo 95, yellow beans -selian 13, njano uyole; sugar beans – masipenjele

The prices of common beans continue to decline among the selected countries. The pace of the decline is faster in Tanzania, closing the gap between the domestic prices and those reported in Kenya and Uganda.

Fertilizer Developments

Fertilizer prices, selected countries (urea fertiliser)

AMO: Own calculations based on multiple sources; AfricaFertiliser.org, World Bank (world price) and Grain SA (South Africa).

- Robust global demand has put upward pressure on world prices which averaged US$496/Mt in July for benchmark urea fertilizer, up from US$421/Mt in June

- Significant data gaps on fertilizer prices in the region make it difficult to track price trends

- Prices in South Africa are increasing with international prices plus transport costs and margins, to US$707/Mt in July, up 20% from June.

- In contrast, prices in Uganda declined for two consecutive months reaching US$685 in July

- Prices in Malawi continue to rise, increasing the gap between domestic prices and global prices as well as those of other countries within the region, reflecting forex challenges for imports (see annexure)

Farmgain Africa.