The market price for maize grain in Kampala has experienced a decline, plummeting from Ugx. 1300/kg to a range of Ugx. 1200 – 1230/kg, as numerous traders procured and processed maize for the Sudanese transit merchants. Conversely, the price of maize flour has escalated from Ugx. 2000/kg to Ugx. 2200/kg at the wholesale level.

The wholesale price for grade 1 ricequality from Tanzania has recorded an uptick, now standing at Ugx. 4400/kg, while other varieties remain considerably more affordable, priced between Ugx. 4100 and 4300/kg.

The initial harvesting phase for the second and final season of 2025 has commenced, particularly benefiting early-season farmers. Reports indicate that freshly harvested maize has begun to appear in the rural production markets.

The supply of groundnuts from Busoga started, leading to a decrease in the general market price for red beauty groundnuts in Kampala. In contrast, a robust supply of white groundnuts from Northern Sudan has rendered them cheaper than usual, now priced at Ugx. 3800/kg at wholesale. Similarly, the Soya bean harvest has prompted a reduction in market prices, with current values ranging from Ugx. 1700 to 2000/kg, contingent on supply.

As the demand for beans escalates, their market price has gradually risen to Ugx. 2400 – 2500/kg in the past week, up from Ugx. 2200 – 2300/kg. Sugar beans are in higher demand, priced at Ugx. 3000/kg, while yellow beans are fetching Ugx. 2800 – 2900/kg, and short Nambale beans are listed at Ugx. 2700 – 2800/kg. A notable reduction in the retail prices offered can be attributed to the substantial volumes made available for resale.

Farmgain Africa.

African Market Observatory (AMO) Price Tracker October

Key Development

In Malawi close to 20% of the population is facing hunger until the next harvest in March 2026; state of disaster declared in 11 of 28 districts following drought ; a maize export restriction was enforced; and a US$45 million emergency food funding granted by the World Bank

The latest reports confirm that La Niña conditions emerged in September 2025 and are expected to last into early 2026. Estimated to be a weak-to-moderate event, it is still likely to bring dry weather conditions to parts of East Africa and above-average rainfalls for Southern Africa as well as flooding

Maize prices in Nairobi and Dar es Salaam continue at very high levels while there is an overall maize surplus in the region

Rice prices in East Africa increased to around three times the benchmark Thailand price

World food prices decline for a second consecutive month.

Zimbabwe addition

As of this Price Tracker, we are adding Zimbabwe to the markets we track.

Zimbabwe is a mid-sized maize producer in Southern Africa, generally ranking below South Africa, Zambia and Malawi and often reliant on imports. Maize is the national staple (white maize) and also used in agro-industrial processes (yellow maize), with annual consumption around 2 million tons.

Production is highly rainfall-dependent and fluctuates sharply between surplus and deficit years, with yields constrained by high input costs such as fertilizer.

Food security is supported by the Strategic Grain Reserve managed by the Grain Marketing Board (GMB).

Imports come mainly from South Africa – a GM maize producer – and Zambia, even though Zimbabwe is generally a non-GM country, meaning prices are above and track South Africa prices.

The El Niño-induced drought of 2023/24 reduced maize output by more than half, prompting a national disaster declaration. Despite this year’s stronger harvest forecast the government lifted the maize import ban

In parallel, the Government issued rules requiring processors to source at least 40% of their annual supply of grain, oilseed, and related products from local suppliers starting in April 2026.

Soybean production is limited relative to demand, requiring imports for feed and processing.

Common beans are widely grown by smallholders and supplemented by imports, while rice is almost entirely imported.

Fertilizer is fully imported, leaving domestic prices exposed to regional and global market trends.

Maize developments

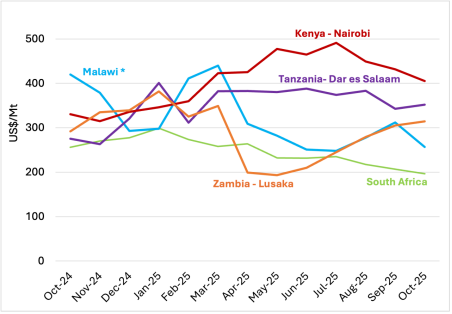

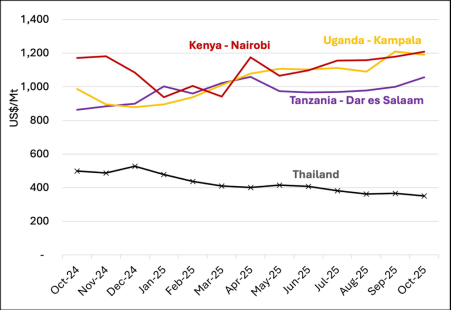

Figure 1: Maize prices, selected ESA countries

1 – Source: AMO based on price tracker data from multiple sources. *Malawi prices received in local currency and converted using the parallel exchange rate from November 2024 to October 2025

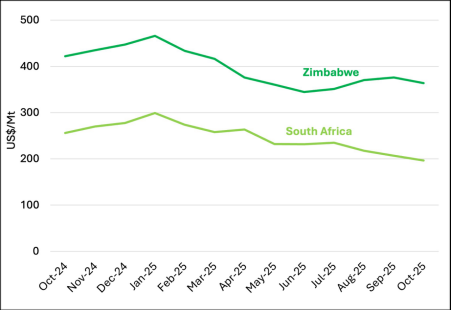

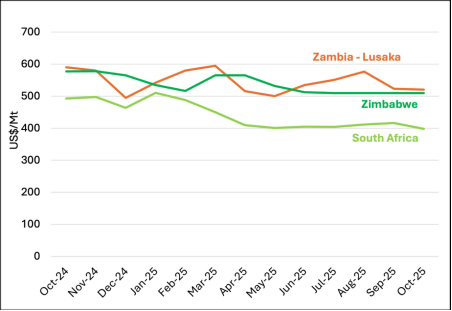

Figure 2: Maize prices, South Africa and Zimbabwe

2 – Source: AMO based on price tracker data from multiple sources.

Zambia maize prices continue to increase, now at US$315/Mt, towards prices in East Africa indicating continued exports given estimated surplus of 1.2 million Mt

Despite an improved harvest in 2025, Malawi faces maize shortages in the range of approximately 600th Mt to 800th Mt

The deficit has been attributed to below average production in southern parts of the country, given low rainfall and insufficient supply of fertilizer

Imports to meet deficit have begun, including from Zambia, while prices at the parallel exchange rate have dropped to US$256/Mt from US$312

Kenya maize prices declined further to US$405/Mt as the harvest started, yet remain the highest amongst the AMO selected countries and approximately 20% above October 2024

Tanzania has high prices, around US$350/Mt in Dar es Salaam, while prices in the main south-west producing area are under US$250/Mt with a good harvest and estimated surplus of 1 million Mt available for export.

The National Food reserve agency NFRA recently announced a tender for 500,000 tonnes of maize for a minimum price of TSh 850 /Kg (US$345/Mt)

Zimbabwe revised production estimates downwards to 1,800th Mt. This contrasts with the USDA estimate for production of 1,300th MT and for an import need to meet a 700th Mt deficit

Given South Africa’s bumper harvest and Zimbabwe being open to GM maize, Zimbabwe’s prices are substantially higher than South Africa, with a difference of US$197Mt

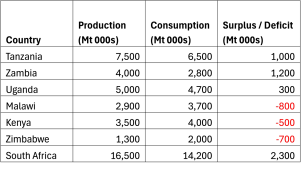

Table 1: Maize demand and supply balances, selected ESA countries

3 – Notes: Production/supply estimates not inclusive of carry-over stocks from previous year. Estimates based on AMO calculations drawing on various sources: USDA; Agri Intelligence Africa; FEWS Net; The Malawi Vulnerability Assessment Committee (Mvac)

With 2025 production in, Zambia has recovered and Tanzania sustained good production meaning surpluses to meet deficits in neighbours

The substantial regional surplus in East Africa contrasts with the ongoing high prices in Nairobi and Dar es Salaam, around double international prices

South Africa’s surplus is in line with the norm, meaning prices at export levels, and with exports to Zimbabwe and into deep sea markets

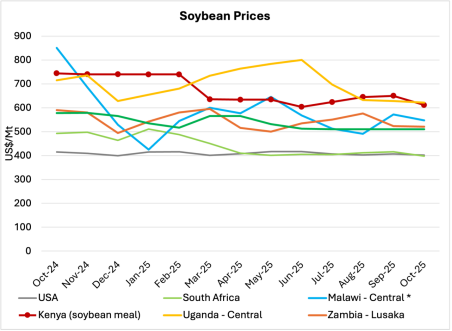

Soybean developments

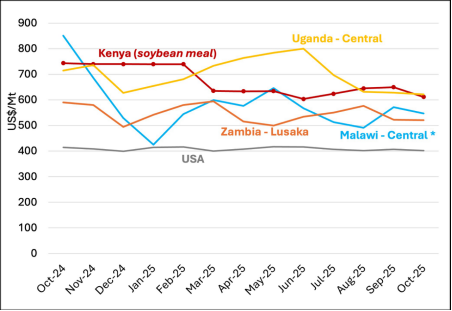

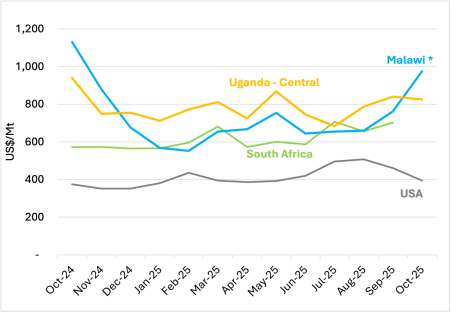

Figure 3: Soybean prices, selected ESA countries

4 – Source: AMO based on price tracker data from multiple sources. *Malawi prices received in local currency and converted using the parallel exchange rate from November 2024 to October 2025, as discussed.

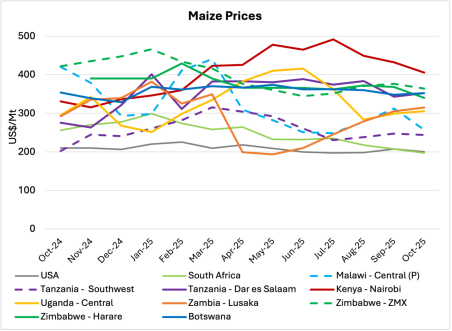

Figure : Soybean prices, Zambia, Zimbabwe and South Africa

5 – Source: AMO based on price tracker data from multiple sources

Kenyan average soymeal prices dipped slightly in October by 6% to US$612 /Mt versus the previous month

Uganda prices level out their descent, down 13% since June (US$800/Mt vs US$622/Mt in October)

Malawi prices (with parallel rates) again above Zambia and the latter very much in line with Zimbabwe (see also chart in appendix )

South Africa practically equal to USA benchmark

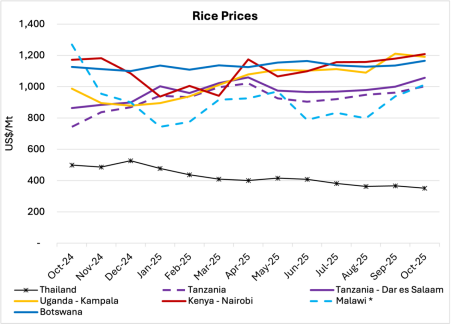

Rice Developments

Figure 5: Rice prices, selected ESA countries

6 – Source: AMO based on price tracker data from multiple sources, Thailand price is from the World Bank.

International rice prices continue to decrease ahead of the main harvest in main exporting countries while prices in East Africa continue upwards, meaning prices in Nairobi and Kampala are now three times the Thailand price

Thailand benchmark fell further to US$351/Mt in October

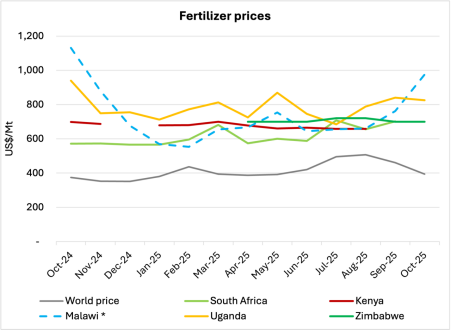

Fertilizer developments

Figure 6: Fertilizer prices, selected ESA countries

7 – Source: Own calculations based on multiple sources; World Bank (world price) and Grain SA (South Africa). * Malawi prices received in local currency and converted using the parallel exchange rate from November 2024, as discussed here.

International urea prices in October are down 14% compared to September and 22% from their 2025 peak of US$508/MT in August.

Prices in Uganda and Malawi continue to trend upward however, widening the margin relative to the international benchmark.

Detailed price charts – Selected ESA countries & International Prices

8 – Source: AMO based on price tracker data from multiple sources, * Malawi prices received in local currency and converted using the parallel exchange rate from November 2024 , as discussed here. South Africa is SA Futures Exchange price; USA is fob prices from SAGIS.

9 – Source: AMO based on price tracker data from multiple sources, * Malawi prices received in local currency and converted using the parallel exchange rate from November 2024, as discussed here. South Africa is SA Futures Exchange price; USA is fob prices from SAGIS.

10 – Source: AMO based on price tracker data from multiple sources, * Malawi prices received in local currency and converted using the parallel exchange rate from November 2024, as discussed here. World price is from the World Bank.

11 – Source: Own calculations based on multiple sources; AfricaFertiliser.org, World Bank (world price) and Grain SA (South Africa). Malawi prices received in local currency and converted using the parallel exchange rate from November 2024, as discussed.

Regional traders demanding for maize grain. Week 49

Maize grain price gradually increases as regional trade from neighboring East Africa markets intensify their purchase. A number of South Sudanese traders pitched camp in Soroti and other major markets buying maize flour. Trade agents are buying maize and milling it for their requrement. In Kampala the maize price increased from Ugx.1050-1100/kg to Ugx.1150-1300/kg at wholesale.

In the western region, the Rwandan trading community found food cheap in Uganda and are currently buying maize grain, matooke, irish potatoes delivered to Rwanda via Katuna border post. In Kamwenge, cross border traders bought maize at Ugx,1120/-1130kg.Others ventured “westwards” to Kibaale,Mubende,Kiboga and Kyankwanzi.

The second season harvest harvest of the year 2025 has started. Parts of Kyankwanzi reported flesh maize grain at Ugx.800/kg wholesale while the old stock maize at Ugx.1000/kg.

Weekly Market Summary. Week 45

This week (3rd to 8th November,2025) minimum trading activities continued to take place at the regional border trade hub of Busia. Maize grain was offered at Ugx.1100/kg w/s. Supply was delivered mainly from northern Uganda via Dokolo Lira trade route to the border town. Good maize grain supply was reported within Kenya but also cheaper maize grain was received from Tanzania before elections. An estimated 700Mt of assorted bean varieties were delivered daily to Kenya via the Produce dealers market at Busia. The market received newly harvested beans from the Western region especially Mubende, Hoima, Kagadi and Kabaale.Yellow beans as…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

October Market Outlook

Maize price registered very low changes during the month of October especially in the peri-urban locations, In Kampala major market, low demand for maize grain was reported specifically from the millers. In the countryside, similar trends were reported with maize grain offered at low market price between Ugx.900-1300/kg. Low cross border trading we likewise reported at Busia-Uganda/Kenya border post because cheaper maize grain and cereals was delivered from Tanzania & Ethiopia respectively to Kenya. High beans price offers were registered in Arua, Nakapiripirit and Kabale where traditional grain production is low. The rainfall in several locations countrywide affected the quality of…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

African Market Observatory (AMO) Price Tracker

Key Developments EAT Lancet report on food systems (see also) and G20 Food Security resolution highlighted the importance of market data and actions for fair markets We find food prices remain high and volatile in East and Southern Africa and cross-border markets continue to work very poorly Good maize harvests, especially in Zambia, have moderated prices somewhat across the region, although prices remain above US$400/Mt in Nairobi. Despite a much better harvest in 2025, Zimbabwean domestic maize production still falls short of national demand and the import ban imposed has now been lifted Soybean and rice prices in East Africa remain extremely high…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

August Market Outlook

The culmination of the initial short harvest season transpired in August; however, the supply of numerous items had been previously recorded in June and July. A significant portion of the commodities is presently held in the custody of the trading community, which consists of rural assemblers, transit traders, and stockists. Many harvested commodities have recorded their lowest price this season and are already beginning to ascend as stocks continue to dwindle. A substantial quantity of beans has been delivered to the market from various production locations across the country. Freshly harvested beans have finally been documented from the western and…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

May Commodity Market Price Outlook late edition

May Commodity market report(1)._late editionDownload

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

May Commodity Market Outlook

The initial indications of the seasonal first harvest of beans were recorded in May 2025. Farmers who cultivated beans and maize early March commenced their harvest, particularly in the central, western, and eastern regions. The supply of Matooke and fresh cassava to the market surged in May, reflecting the successful harvest of these commodities and subsequently leading to a decline in their market prices when compared to data collected in April. In the dry maize grain market of Kisenyi, Kampala, maize was offered at a premium price of Ugx. 1,530/kg wholesale. Meanwhile, some fresh maize on the cob entered the…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

April Commodity Outlook

Increasing commodity prices were registered during the month of April. Stockists held on to their stocks as they speculated for the highest margin from the 2nd seasonal harvest that came late in January/February. More bulking of grains and pulses was recorded, especially in the northern region, however, it was reduced by unusual transit buyers from Rwanda who ventured into the region in search for maize grain at the onset of the year. The main maize market in Kampala recorded in the opening week at Ugx.1,380/kg in Kisenyi /Kafumbe Mukasa Road Market. It gradually increased in the weeks that followed to Ugx.1,550/kg…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

March Commodity Outlook

The maize grain price increased steadily during the month of February. It was influenced by March Commodity Market Report. Less commodity supply was reported delivered to market during the month of March. Land preparation and planting activities were visible in some production locations, especially the bimodal areas that registered some rainfall towards the end of March. Nevertheless, preparations for planting and initial clearing of gardens were reported in the unimodal locations such as Karamoja where the weather remained hot and dry. Given the off-season nature, commodity prices increased drastically because of limited supply. Maize grain in Kampala’s main market increased…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

Real-time price trends for 23+ commodities across Uganda, Kenya, and Tanzania

Expert Tools

Unlock actionable insights for smarter farming, trading, and policy decisions

Member-Only Resources

From fertilizer price trackers to cassava value chain guides, we empower your success

February Commodity Outlook

The maize grain price increased steadily during the month of February. It was influenced by several factors including the opening of the first school term, delay in the second annual seasonal harvest due to shift in the weather Pattern and also the regional demand especially from Rwanda. The grain market in Kampala registered maize at Ugx1180-1220/kg wholesale. When compared to the previous year 2024, the second harvest season arrived late, was priced twice higher and met demand for maize from Sudanese & Rwandan traders. Other commodity prices were similarly raising due to scarcity such as beans which had been harvested…

Member Access Only 🙂

Unlock Exclusive Insights—Subscribe Today!

Gain full access to Farmgain Africa’s restricted content, including premium market analysis, food security reports, and value chain strategies designed to boost your agribusiness.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.